Q3 2024 has been a corrective period for the dapp industry, marked by growth in industry usage while other key metrics faced downturns. Despite a 70% increase in daily active wallets (UAWs), sectors like DeFi, NFTs, and overall trading volumes saw notable declines. This shift reflects a market recalibration, raising questions about what the future holds.

To better understand the trajectory for Q4 and beyond, it’s essential to analyze the trends that shaped Q3. This report dives into the key developments and challenges the dapp industry faced, offering insights that will help navigate the evolving Web3 landscape.

Key Takeaways

- In Q3 2024, the dapp industry experienced a significant 70% increase in usage compared to the previous quarter, with daily Unique Active Wallets (UAWs) reaching 17.2 million.

- The AI-driven dapps in the “Other” social category led the Web3 industry’s growth, recording a 71% increase in daily UAWs, now averaging 4.3 million users.

- DeFi continued its downward trend, with a 5% decline in total value locked (TVL), dropping to $160 billion.

- Sui and Aptos emerged as standout performers in the DeFi space, both seeing TVLs surpass $1 billion, representing nearly 80% growth for each chain.

- The NFT sector faced significant challenges, with trading volume plummeting to $1.6 billion, the lowest recorded this year.

- OpenSea reclaimed its leadership in the NFT marketplace, ranking first in trading volume, number of sales, and active traders.

- Despite overall positive market trends, the Web3 space saw $427 million in losses due to exploits and hacks, a slight decrease of just 0.7% from the previous quarter.

Table of Contents

- A record-breaking quarter for dapps

- DeFi drops to $160 billion

- Market correction in the NFT sector

- Exploits and hacks: a persistent threat to Web3 security

- Closing words

1. A record-breaking quarter for dapps

The dapp industry has continued its impressive upward trajectory in Q3 2024, reaching unprecedented levels of engagement. Daily unique active wallets (UAWs) surged to an all-time high of 17.2 million, reflecting a remarkable 70% increase from the previous quarter.

All sectors within the dapp industry experienced significant growth, contributing to this bullish trend. However, the AI-related dapps have been the standout performers, showing a 71% growth compared to the previous quarter. These dapps now average nearly 4.3 million daily UAWs, underscoring the rising excitement surrounding AI technologies.

Notable dapps like DIN and Alaya AI have emerged as key drivers of this surge, as users increasingly interact with AI-powered solutions. For a deeper analysis of this sector’s growth, check out our AI Mini Report for a detailed breakdown of the top-performing AI dapps and trends driving this performance.

While gaming remains the dominant sector, its share of the overall dapp industry has slightly declined, mirroring trends seen in DeFi and NFTs. Despite this decrease in market share, gaming continues to lead in user activity, maintaining its stronghold in the industry.

The social sector, on the other hand, held steady this quarter, maintaining its influence and appeal among dapp users.

Several key dapps have dominated the conversation this quarter, each contributing to their respective sectors’ growth:

HOT Game: A new, gamified wallet built on Telegram using the Near blockchain. Telegram-based dapps, along with TON, have seen a surge in popularity, drawing in large communities and reshaping how users interact with dapps through social platforms.

CARV: A revolutionary social dapp that is building the largest modular data layer for both Gaming and AI. CARV has redefined data privacy, ownership, and value, ensuring that individuals retain full control over their data, all while paving the way for data to generate value in an entirely new manner.

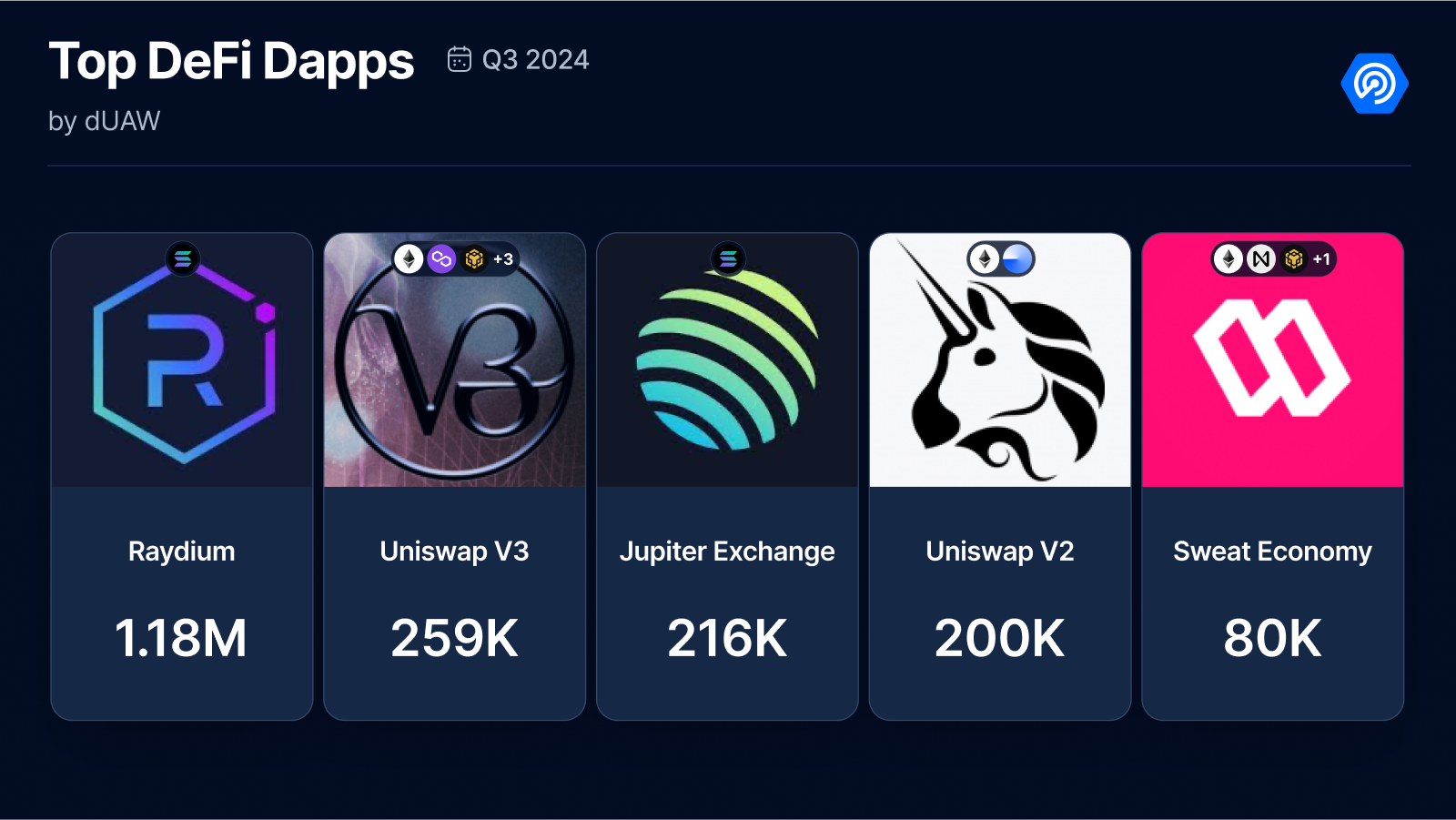

Raydium: A decentralized exchange (DEX) that gained substantial traction this quarter, particularly for memecoin trading. Raydium’s heavy use in the DeFi sector has placed it at the top of the charts for decentralized exchanges this quarter.

Pixels: As the most talked-about and most played game this quarter, Pixels has captured the attention of the gaming community, offering an immersive experience that continues to attract daily active users.

2. DeFi drops to $160 billion

The DeFi sector faced a challenging Q3 2024, with total value locked (TVL) continuing its downward trend. By the end of the quarter, TVL had dropped from $168 billion in Q2 to $160 billion, reflecting ongoing market uncertainties despite some positive regulatory developments.

Ethereum remains the dominant force in the DeFi space, commanding a TVL of $95 billion in Q3 2024. However, this marks a significant 20% decrease from Q2, despite the U.S. SEC’s surprise approval of the spot ETH ETF, which many expected to boost the market.

While Ethereum saw a decline, the real winners this quarter have been newer layer-1 blockchains like Sui and Aptos. Both platforms recorded impressive TVL growth, with each seeing a 78% increase since Q2. This surge catapulted them into the ranks of top DeFi chains, signaling growing investor interest in alternative ecosystems that offer innovative solutions and faster transaction speeds.

Among the top-performing DeFi dapps this quarter, Raydium and Uniswap V3 stood out, both witnessing substantial increases in unique active wallets (UAWs). This spike in activity is largely attributed to the continued popularity of memecoin trading, which remained a dominant trend throughout Q3 2024.

3. Market correction in the NFT sector

The NFT industry faced significant challenges in Q3 2024, marking a stark contrast to the positive performance of the previous quarter. After experiencing one of its best quarters since early 2023, the NFT market took a notable hit, with trading volume plummeting to $1.6 billion, representing a sharp 60% decrease from Q2. Similarly, NFT sales dropped to 11.5 million, a 23% decrease, underscoring the market’s contraction over the past three months.

NFT marketplace landscape

The NFT marketplace landscape also saw substantial shifts this quarter. OpenSea emerged as the dominant platform across several key metrics, including trading volume, number of sales, and active traders. This marks a significant rebound for OpenSea, which had been struggling just a few months ago but has now fully regained its top position.

In contrast, other leading marketplaces like Blur and Magic Eden have faced steep declines. Blur, which was the leader in trading volume in Q2, saw a staggering 78% decrease this quarter. The platform’s drop can be attributed to the winding down of its airdrop incentives, which had previously fueled high trading volumes. Magic Eden also experienced a substantial dip in activity, largely due to its decision to eliminate royalties, driving creators and traders toward OpenSea. Additionally, the Bitcoin Ordinals hype seems to have vanished, and Magic Eden was extremely popular in that.

Top NFT collections

The top NFT collections by trading volume remained relatively stable compared to the previous quarter, though a few collections made notable gains. Sorare and Guild of Guardians were two standout performers that entered the top five for the first time this quarter.

Sorare experienced a surge in popularity, driven largely by its integration with UEFA Euro 2024, an event that attracted over 5 billion viewers and saw 2.6 million spectators attending the matches. The global attention on football has boosted the trading volume of Sorare’s sports-related NFTs, making it a key player this quarter.

Guild of Guardians, a highly popular Web3 game available on Google Play and the App Store, also made significant gains. Its accessibility on mobile platforms has helped it capture a wide audience, cementing its position as one of the most actively traded collections. More in-depth insights on this game will be covered in our upcoming Q3 2024 Games Report.

4. Exploits and hacks: a persistent threat to Web3 security

Exploits and hacks continue to pose a serious challenge to the Web3 industry. In Q3 2024, the sector saw $427 million in losses due to security breaches, according to data from the REKT Database. This represents only a 0.57% decrease from the previous quarter, indicating that the problem remains largely unsolved.

Ethereum was hit the hardest, accounting for 57% of all reported incidents, reinforcing its status as a prime target for attackers due to its large user base and TVL. BNB Chain followed closely with 24% of the attacks. Other incidents occurred across a variety of networks, including Ronin, Avalanche, and Arbitrum. These figures highlight that no blockchain is immune to security vulnerabilities, making cross-chain security an ongoing priority for the entire industry.

This quarter saw several high-profile hacks that contributed significantly to the overall losses:

- WazirXIndia Exchange Multisig: In the largest exploit of the quarter, the multisig wallet of the exchange was compromised, resulting in the loss of $230 million worth of assets in ETH.

- On August 21, 2024, a victim lost $55.43 million in DAI after falling prey to a phishing attack that compromised their DeFi Saver Proxy, allowing the attacker to drain all funds.

- In September 2024, Singapore-based centralized exchange BingX was hacked, losing approximately $52 million from its hot wallets.

- On September 3, 2024, Penpie, a yield protocol, was exploited for $27 million due to a reentrancy vulnerability in its smart contracts.

- Indodax, an Indonesian crypto exchange, was hacked on September 10, 2024, resulting in losses of about $22 million across multiple cryptocurrencies. The methodical attack targeted the exchange’s hot wallets, once again underscoring the vulnerability of centralized exchanges.

As the Web3 space continues to grow, the importance of adopting robust security practices cannot be overstated. Blockchain platforms must address common vulnerabilities such as access control flaws and smart contract weaknesses while also deploying comprehensive threat-monitoring systems.

Equally important is user education. Many incidents stem from phishing attacks or social engineering tactics, which can often be mitigated through better awareness and understanding of security best practices.

For more information on how to protect your assets and stay safe in the Web3 world, check out our resources on scam prevention:

5. Closing words

Q3 2024 has been a pivotal quarter for the dapp industry, marked by impressive growth in some sectors and significant challenges in others. The rise of AI dapps and the continued dominance of gaming highlight the dynamic nature of the space, with 17.2 million daily UAWs setting new engagement records. However, the DeFi and NFT sectors have seen notable declines, revealing the shifting tides of user interest and market momentum.

The NFT market, once a powerhouse of innovation and excitement, struggled with declining trading volumes and sales, though platforms like OpenSea regained leadership and emerging collections like Sorare and Guild of Guardians brought renewed energy. In DeFi, the rise of newer chains like Sui and Aptos indicates a growing appetite for alternatives to Ethereum, while memecoin trading fueled increased activity on platforms like Raydium and Uniswap V3.

However, alongside these growth narratives, the Web3 industry continues to face serious security challenges. With $427 million in losses due to exploits and hacks, it is clear that robust security measures and user education remain paramount for the industry’s long-term sustainability.

As we look ahead, the next quarter promises further evolution. The growing integration of AI, the potential rebound of NFTs, and the ongoing development of decentralized finance will continue to shape the future. But with each opportunity comes the need for vigilance, whether in securing assets or adapting to new trends.

Q3 2024 was a quarter of both growth and reflection, and as the Web3 space matures, the balance between innovation, user engagement, and security will be critical to its success.